What is Estate? Why do you need to plan it?

“Death and Tax are certain”You are working hard to build your wealth assuming your kids will be able to enjoy it when they grow-up and you are gone from this planet. Think again! How will CRA react when the next-generation ‘inherits’ this fortune.

An inheritance or Estate Tax: Even though there is no inheritance-tax per se, but indirectly tax is actually charged to every penny found in the ‘treasure’ before it’s granted to your loved ones. And those taxes pile-up much higher than you can imagine.

Definition of Estate: All the money and property owned by a particular person, especially at death.

Types of Taxes due on very last return

RRSP/RRIF: Parking your savings during young-days in RRSP and using the same later in smaller chunks saves significant tax. Until it no longer stands true due to the fact that you are not there anymore. On the very last tax return, the whole money from RRSP/RRIP is added back as regular income, termed as income-inclusion.

Let's do some math here on how much tax you may owe when transferring RRSP money to your family. Assuming you contribute maximum as per CRA limit:

| Tax due on RRSP | |

|---|---|

| Total maximum contribution in 30 years | $588,000 |

| Growth w/ 4% average ROI | $1,250,000 |

| Tax due at Age of 65 | $630,000 |

| Assuming, Withdraw $120,000 yearly next 10 years | |

| Tax due at age of 75 ( All funds are 100% taxable including growth) | $175,000 |

Disclaimer: Total RRSP balance may vary depending upon how much actually contributed yearly and ROI depends upon choice and return of underlying instruments under the registered plan.

To summarize, RRSP is not really a tax-free money. A large tax bill is associated at your very last income tax return which needs to be handled carefully.

Real Estate Property: Real-Estate is the all-time favorite financial instrument most people like to use for building long-term assets, especially with the purpose of passing the same to the next generation. Any capital gain on real-estate, except your primary home, is taxable. Like a countryside cottage kept for amusement or invested in a condo to earn rent, appreciation of fair market value falls under capital gain. . Even if there is no real ‘sell’ transaction was done in the market, CRA assumes the property is sold on the day of the owner’s death. The fair-market-value is treated as the price to support the tax calculation.

| Tax due on Real Estate | |

|---|---|

| Average cost of a house you buy today | $600,000 |

| Growth with 6% average over 30 years, market value would be | $3,500,000 |

| Capital Gain (CRA assumes as-if property was sold on death) | $2,290,000 |

| Assuming, no other asset or money part of taxable income | |

| Tax on 50% of Capital Gain due | $730,000 |

Disclaimer: Total tax due on real-estate depends upon how many properties accumulated over years, their adjusted cost and market value at the time of death. Average Growth may be much higher than assumed in this sample table depends upon the location/size of the property along with other market factors

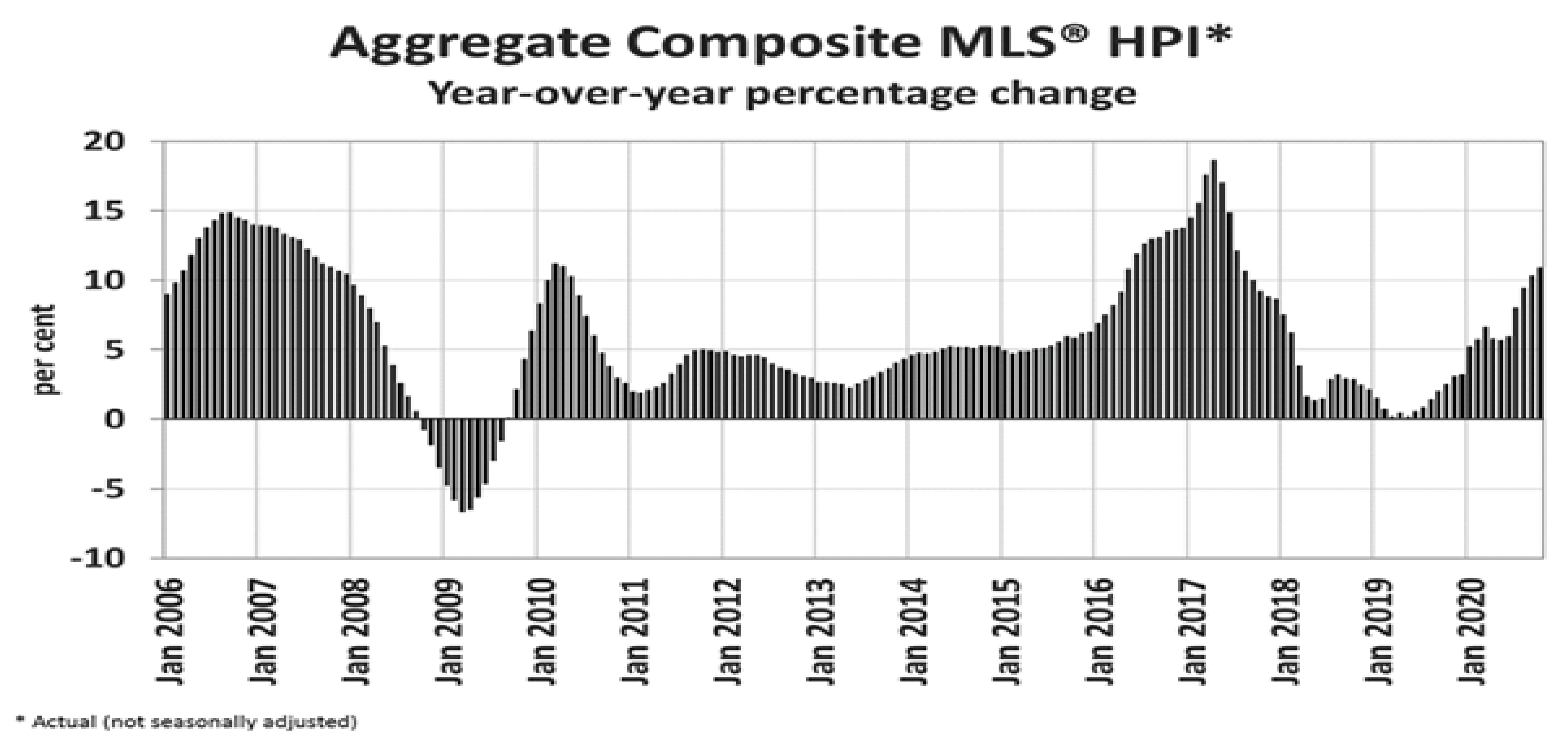

In the last 15 years, the yearly growth rate for real-estate has been fluctuating like a roller-coaster between 18% to negative -5%. (Refer MLS HPI graph). This is a huge tax liability and must be planned well in advance to avoid the scenario where the property had to be sold rather than enjoyed for coming generations.

Source: https://creastats.crea.ca/en-CA/ [The Canadian Real Estate Association]

Even for the property, you have inherited from your ancestors, once it’s transferred to your children, the tax has to be paid based on the difference between market values i.e. at the time when you acquired from your parents vs. when your loved ones obtain from you.

Investments : Savings under non-registered accounts have no regulated limits. It's your tax paid money but still attracts tax on the appreciation. From Guaranteed Investment Certificates (GIC), Mutual Funds, Bonds to Stocks, Exchange-traded funds (ETF) and more; There are several financial instruments available to balance risk vs. return and tax is calculated differently for each type of gain.

| Tax due on Investments | |

|---|---|

| Assuming $5000 yearly investment over 30 years | $150,000 |

| Growth w/ 7% average ROI | $500,000 |

| Capital Gain | $350,000 |

| Assuming, no withdrawals were made, half of the gain is taxable | |

| Tax due (50% of capital gain) | $60,000 |

Disclaimer: All financial instruments can be managed under registered or non-registered accounts. The sample table assumes average savings and ROI combined with high performing growth funds for 30 years. The gain may be adjusted against adjusted-cost-base (ACB) for charges/dividends etc.

The magnitude of tax liability really depends upon the size of the investments in total. But it’s true that a significant amount of capital gain will be added to your last taxable income.

Probate (Legal) Fee : Here comes the boring stuff! Legal paperwork. Before your wealth can be transferred to your family, it has to go through a legal process. The government ensures that the assets are rewarded to the rightful owner and all the dues are paid. A ‘Last Will and Testament’ helps the overall processing but still attracts a legal fee , known as ‘probate fee’ is charged to ensure that all necessary documents are genuine and no forgery is involved.

Each province has a different fee rate prescribed. If your estate value is $5 million, the fee in Ontario could be $75000 or in Nova Scotia upto $85,000.This fee has to be paid by your family before inheriting all the hard earned money you left for them.

| Probate / Legal Fee | |

|---|---|

| Total Assets/Estate Value (Inclusive of RRSP, Real-Esate & Investments) | $4,400,000 |

| Ontario fee 1.5% of value | $66,000 |

Funeral Cost : Anyone who is gone gives a major setback to the nearest family. There is absolutely nothing which can fulfill that loss. Over and above, that the final-cost has to be arranged by family members. Depends upon how complex are the religious rituals as well as how fancy is the funeral home, this cost can range from $5000 to $12,000.

Putting it all together: Let’s see how much actually is due on very last tax return:

| Tax due at age of 75 ( All funds are 100% taxable including growth) | $175,000 |

| Tax due on Real Estate(Tax on 50% of Capital Gain due) | $730,000 |

| Tax due on Investments(50% of capital gain) | $60,000 |

| Probate / Legal Fee | $66,000 |

| Funeral Cost | $5000 |

| Grand Total Dues | $1,036,000 |

Disclaimer: Taxes for each asset is calculated separately; Combining all of them together, within a single income-tax return, would result in higher tax liability. Sample figures merely project how income-inclusion works; Actual tax liabilities are to be calculated by the licensed accountant.

“Death and Tax are certain”

When things are variable and change based on life situations, “Death and Tax are certain”. Putting aside another million dollars will prove counterproductive because all your life long built assets are taxable. If you really want to give them to your children, estate planning is unavoidable. An intellectual strategy will be required to handle this huge liability. We have time-tested game plans that confirm that the next-generation inherits your ‘treasure’ with no pain.

Disclaimer: All figures in the blog are for illustration purposes only assuming an average Canadian lifestyle. Every individual’s financial situation is different and must be assessed carefully to plan an efficient estate to handle tax liabilities consulting with tax experts