Is CPP and OAS enough for Retirement?

If not planned well, retirement days can be difficult.

Every Canadians is aware that basic benefits are granted by Government supported programs including Canada Pension Plan (CPP) and Old Age Pension (OAS).

- But is that sufficient?

- How much will be required to sustain a reasonable standard of living?

- How to determine when to retire?

To obtain answers for these questions it’s important to grasp understanding of few key concepts:

Purpose of CPP and OAS

These programs are designed as ‘starters’ and must not be presumed to fulfill all retirement needs. Government mandated every working Canadian to contribute into CPP as part of their regular income. The objective is to enforce the needs of ‘saving’ for retirement days. The government invests this money in low-risk instruments with conservative potential rate of return before the regular income is paid back post retirement. A large amount should not be anticipated from this source.

Over and above the CPP program, the Government adds OAS as free income.(No contribution required).

Every Canadian is expected to build a solid post-retirement to support all days till rest of the life where CPP and OAS works a supplementary income.

How much will you need post retirement

Whether your financial situation is sound enough to retire-happy or you should be worried because you may outlive your savings; it all depends upon simple math you caf

Nobody can see the future but based on the historical data, in last 25 years, a ‘basket’ of goods & services that cost $1000 in 1995, will need $1562.14 today, Assuming same rate of average inflation (i.e. 1.8%) if reasonable household expenses paid with $5000 today, in next 25 years i.e. by year 2045 the price tag would be $7810.24 for the same.

What is inflation : Decline in the value of money or how much each dollar lost purchasing power every year.

Income Gap

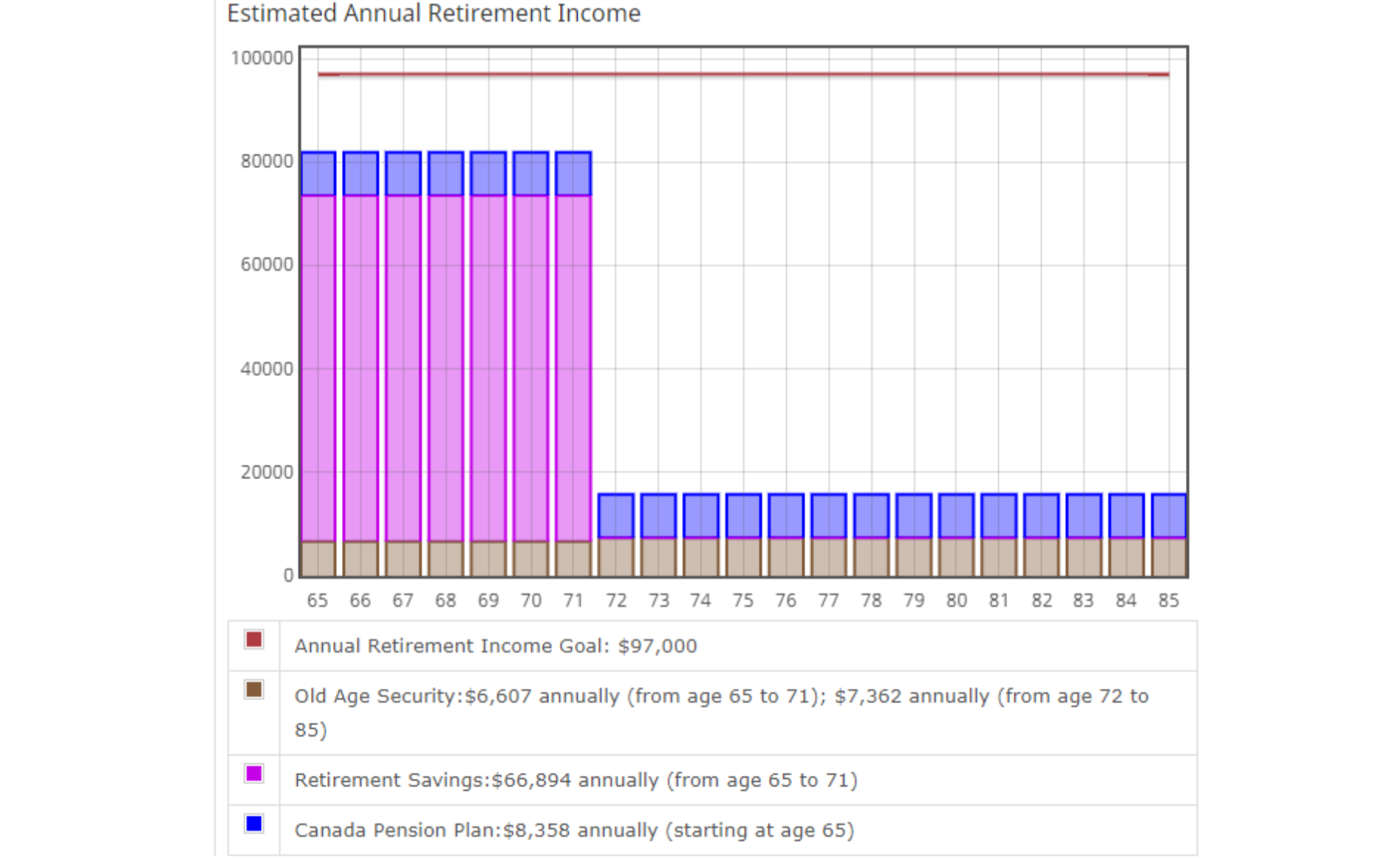

It’s important to figure out how much monthly income will be generated using all government benefits along with your own savings/pensions. Average Canadian age is about 83 years. So the overall need would be around 20 years of more. Currently maximum CPP is $1,175.83 and maximum OAS is $613.53

Using these base numbers you can determine when will you be able to afford to retire. Please use an official retirement calculator to find what’s the expected income gap that CPP+OAS will provide and any other pension plan you have.Retirement Income Calculator

Objective is not to scare you but to educate you before it’s too late to start taking some important decisions about your old days.

Sample : Identified gap figure assuming RRSP plan utilized till the age of 71.Retirement Income Calculator

How to fill the income gap

Bank Deposits bring peace-of-mind but can’t fill the income gap. In fact in some years Guaranteed Investment Certificates (GIC) not able to beat inflation. Stocks are attractive but not everyone's cup-of-tea.

There are many smart and low risk investments opportunities available in the market. For instance, Universal Life Insurance (UL); Although these products are designed by insurance companies, these are considered effective investment vehicles to support retirement income. Equipped with underlying high-performing mutual funds the expected return is much higher as compared to GIC but at the same time the tax-treatment is similar to RRSP i.e. deferred tax.

Segregated funds are another long term investment instrument, which guarantee a larger portion of the principal money and still bring high returns back without losing your sleep.

In summary, Long term investment ( 20 to 40 years) can easily fill this gap and you can happily retire. You just need to start now and start directing your savings to the right product.

Source

https://www.bankofcanada.ca/rates/related/inflation-calculator/

https://www.bankofcanada.ca/rates/price-indexes/

https://www.canada.ca/en/services/benefits/publicpensions/cpp/old-age-security/payments.html

https://www.canada.ca/en/services/benefits/publicpensions/cpp/cpp-benefit/amount.html